Ripple has formally proposed two XRPL amendments, XLS-65 and XLS-66, that may embed fixed-term institutional credit score infrastructure instantly into the XRP Ledger. With it rolling, the validator voting can be now lively following the Rippled v3.1.0 launch in late January 2026.

The framework targets uncollateralized, underwritten lending for regulated monetary establishments, positioning XRPL as a credit score layer relatively than a funds rail. It’s a structural shift that hinges solely on whether or not the amendments can clear an 80% validator consensus threshold.

Why Tokenization Alone Fails And How Doppler Is Fixing It on XRPL

Tokenized property are exploding, however with out lending they keep passive. Actual capital markets want credit score.

XLS-66 brings native lending primitives to XRPL (pooled vaults, fixed-term loans, onchain monitoring).… https://t.co/z29H0TLjrd— 𝗕𝗮𝗻𝗸XRP (@BankXRP) July 2, 2026

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

That threshold stays the important unknown. As of latest monitoring, XLS-65 held roughly 8 validator sure votes, or simply 22.86%, whereas XLS-66 had secured round 7, or 20%. Each figures sit effectively under the sustained 80% assist required over two consecutive weeks for mainnet activation.

Uncover: The Finest Crypto to Diversify Your Portfolio

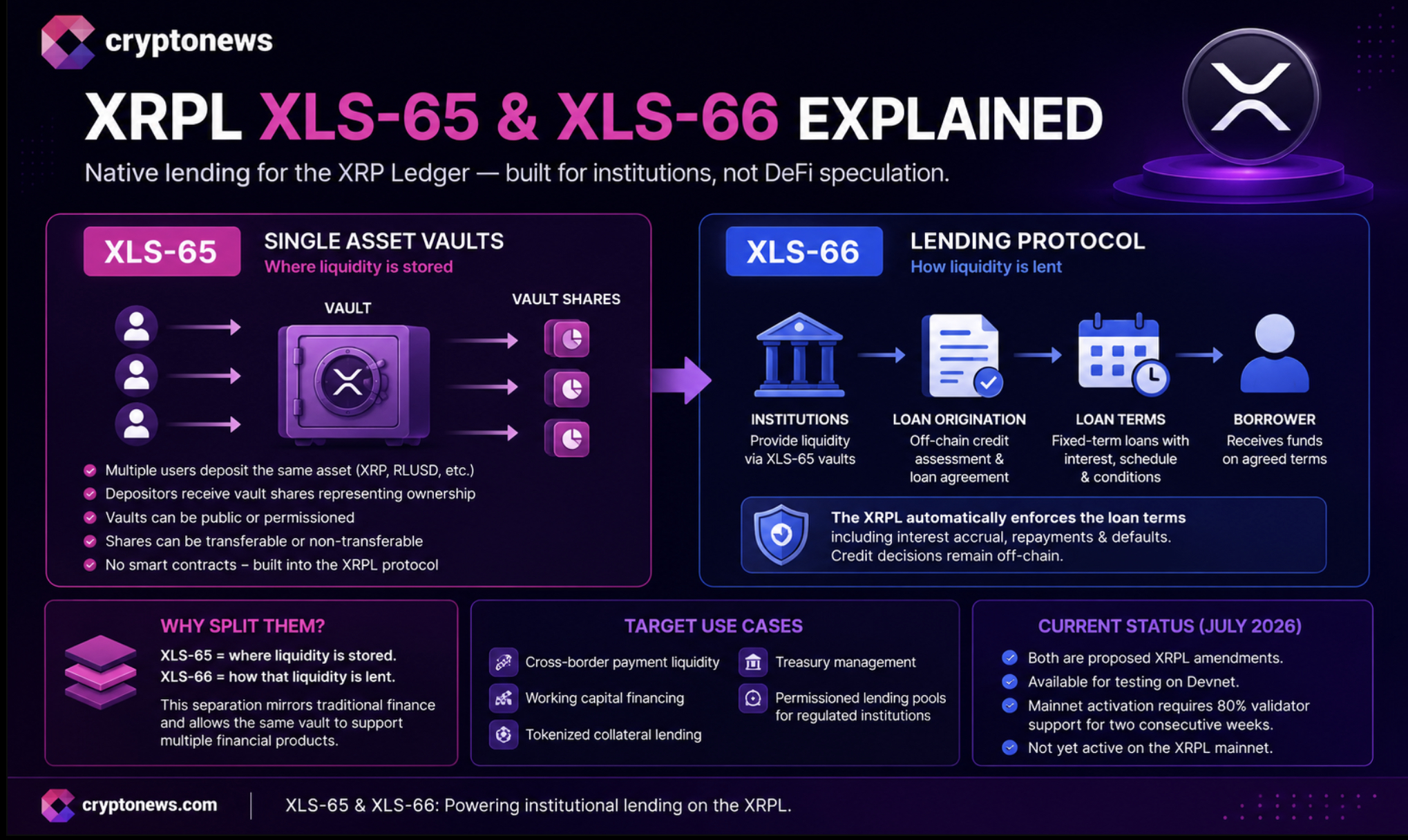

Single Asset Vaults and the Lending Protocol Mechanics

The 2 amendments function as an interlinked system. XLS-65 introduces Single Asset Vaults, permissioned swimming pools the place liquidity suppliers deposit a single token. It holds RLUSD, XRP, tokenized U.S. Treasuries, or different tokenized property, that are held instantly by the vault construction itself. The XLS-65d revision simplified this mannequin by eliminating two beforehand required transactions, decreasing overhead for each depositors and redemption flows.

XLS-66 builds the XRPL lending protocol on high of these vaults, specifying the on-ledger mechanics for mortgage origination, curiosity accrual, amortized reimbursement, and default enforcement through LoanSet, LoanPay, and LoanDelete transactions. Critically, underwriting and borrower credit score evaluation stay off-chain.

With this, institutional credit score desks deal with the chance analysis whereas XRPL manages execution and the mortgage lifecycle. This isn’t Aave-style overcollateralized lending; it’s fixed-term, underwritten credit score prolonged to credentialed counterparties.

The compliance structure runs by way of XRPL’s current permissioned domains, credential verification, clawback mechanisms, and freeze performance. Vault operators can limit participation to KYC/AML-compliant entities on the protocol degree, which is exactly what separates this from open DeFi.

Uncover: The Finest Token Presales

XRP at $1.00: What Activation Would and Would Not Show

XRP is buying and selling close to the $1.00 degree, a psychologically vital threshold that has drawn consideration from technical analysts monitoring a coiling triangle sample with progressively larger lows towards flat resistance.

XLS-65 and XLS-66 activation would affirm XRPL as a viable credit score infrastructure layer, however the demand sign that really strikes value is institutional adoption. Value motion will depend upon whether or not regulated entities deploy capital into RLUSD-funded vaults at scale.

Xrp (XRP)24h7d30d1yAll time

Xrp (XRP)24h7d30d1yAll time

The amendments are at present testable on devnet, and builders can combine towards the lending stack forward of mainnet activation. XRP’s market efficiency within the close to time period shall be formed extra by whether or not validator momentum accelerates towards that 80% threshold than by any single technical degree. The framework is credible; the activation path just isn’t but assured.

Uncover: The Finest Crypto to Diversify Your Portfolio

The submit XRP Ledger Lending Amendments Face 80% Validator Hurdle as Institutional Credit score Layer Takes Form appeared first on Cryptonews.