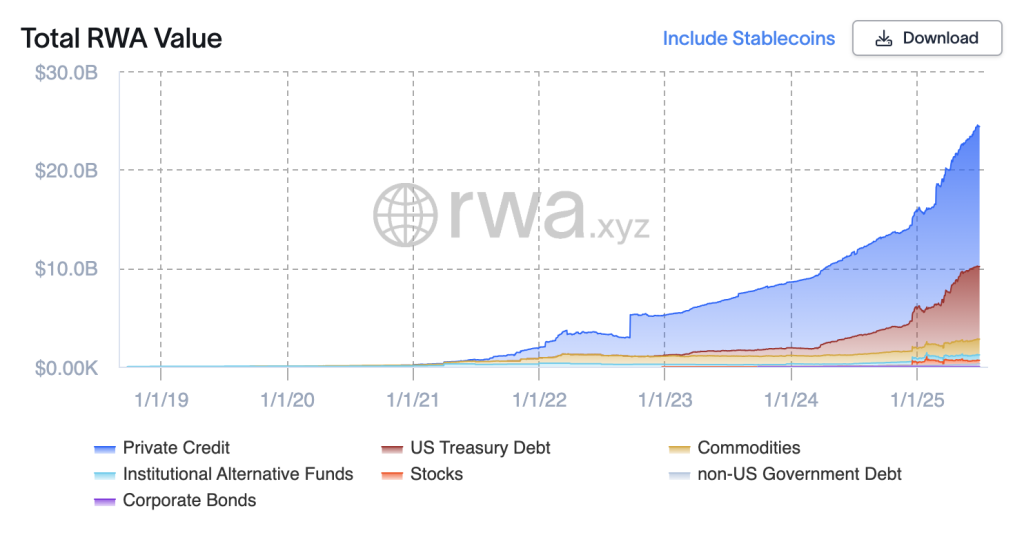

Actual-world asset (RWA) tokens have develop into 2025’s favourite blockchain story. Treasuries, actual property, even whisky casks — round $24 billion price — now sit on public ledgers.

Certainly, the worth on-chain is rising quick, however what actually issues is what’s nonetheless lacking beneath. Authorized uncertainty, tech bottlenecks, and custody blind spots — any certainly one of these may deliver the entire experiment to a impasse.

With billions already on-chain and institutional gamers watching, tokenization has moved past idea, however its foundations are nonetheless fragile. If we don’t repair the fundamentals, the momentum may stall earlier than this factor actually takes off. Who owns what? How does the system speak to itself? And is there anybody really holding the actual asset?

Let’s break down the three greatest challenges holding the sector again and what must occur if we would like this $24 billion market to imply one thing greater than one other crypto “flash-in-the-pan.”

Tokens With out Title

The most important blind spot within the tokenization growth can be essentially the most fundamental: a token isn’t possession, it’s a declare to possession that solely issues if the authorized system agrees.

In just a few forward-looking jurisdictions, like Luxembourg, digital securities now have authorized standing, however a lot of the world nonetheless treats on-chain tokens as representations, not rights. A belief could maintain the underlying bond or property, and the token turns into a digital IOU. On paper, it’s elegant. In courtroom? Not assured.

In a chapter, a choose may deal with a tokenized bond the identical as some other unsecured declare, folding it into the property with no particular precedence. Even in main markets, registry programs for property or securities are nonetheless paper-based, which means there’s no clear option to reconcile digital claims with real-world possession. As for cross-border operations, the issue will get even worse. Enforcement hinges on conflicting authorized doctrines, not code.

On this scenario, I’m positive that regulators ought to construct harmonized definitions of digital property which are transportable throughout borders and enforceable in courtroom. Till this occurs, tokenization stays fragile. To this point, we’re simply giving monetary infrastructure a slick new entrance finish that also depends on old-world belief.

Fragmented Tech and Compliance

Even the place the legislation isn’t a barrier, the expertise nonetheless is. Tokenized property transfer on infrastructure that was by no means designed to interoperate, and it reveals.

Ethereum stays the primary hub, but it surely’s not often the most affordable or most effective. Transactions can price a number of {dollars} apiece, and whereas Layer-2 options like Arbitrum assist, they introduce different issues. Which of them? Liquidity is fragmented, bridging provides danger, and customers should handle separate environments that don’t speak to one another cleanly.

Compliance is simply as fractured. Most token issuers run their very own permission programs — who can maintain a token, who can redeem it, and underneath what guidelines. Meaning even when your pockets handed KYC for one asset, it could must undergo the method another time for one more. The result’s a disjointed market the place each on-chain interplay turns into a brand new onboarding occasion.

What would change that? Shared compliance rails, like ERC-3643, if adopted extensively and aligned with regulation, are a viable method ahead. In any other case, we’re simply rebuilding legacy silos with sleeker instruments.

Information and Custody Threat

Tokenization could also be digital, but it surely nonetheless leans closely on offline details. Each token tied to a bond, a property, or a warehouse wants somebody (or one thing) to confirm that the asset is actual and nonetheless the place it’s speculated to be. That’s the place issues get unclear.

Oracles feed exterior knowledge into sensible contracts: costs, possession adjustments, and funds. However these feeds can lag or fail, and sensible contracts don’t know what’s occurring off-chain. If an replace is late or incorrect, redemptions can freeze or misfire, and in unstable markets, even small delays flip outdated knowledge into actual liabilities.

Custody, in flip, brings its personal dangers. You would possibly maintain the token, however another person holds the real-world asset. If that custodian lacks transparency, correct auditing, or authorized accountability, the token turns into a digital receipt with no proof behind it. Outdoors well-regulated belief banks, custody requirements are everywhere, and traders usually don’t know what sort of safety, if any, they really have.

To repair that, tokenized markets want real-time reserve proofs, stronger oracle requirements, and custodians who’re clear, accountable, and auditable. Among the infrastructure already exists.

Tokenization Solely Works if It Scales

From my perspective, tokenization is already proving itself — in managed pilots, closed programs, and sandboxed rollouts. However that’s not how monetary infrastructure scales. With out authorized alignment and shared compliance rails, this area dangers remaining a patchwork of “gated” corridors.

I’m not looking ahead to the following flashy protocol. I’m presently looking ahead to convergence — lawmakers who outline digital possession clearly and platforms that cease reinventing KYC from scratch.

Disclaimer: The opinions on this article are the author’s personal and don’t essentially symbolize the views of Cryptonews.com. This text is supposed to offer a broad perspective on its subject and shouldn’t be taken as skilled recommendation.

The publish The Tokenization Hype Is Actual — So Are the Three Gaps That Might Stall It appeared first on Cryptonews.